Despite all of the talk about cord-cutting, a new report from Digital TV Research forecasts that the number of pay TV subscribers in North America will continue to increase – despite a small decline in 2013.

The Digital TV North America report estimates that nearly 5 million more subscribers will be added between 2013 and 2020. However, pay TV penetration will drop from 87.0% in 2010 to 83.8% by 2020.

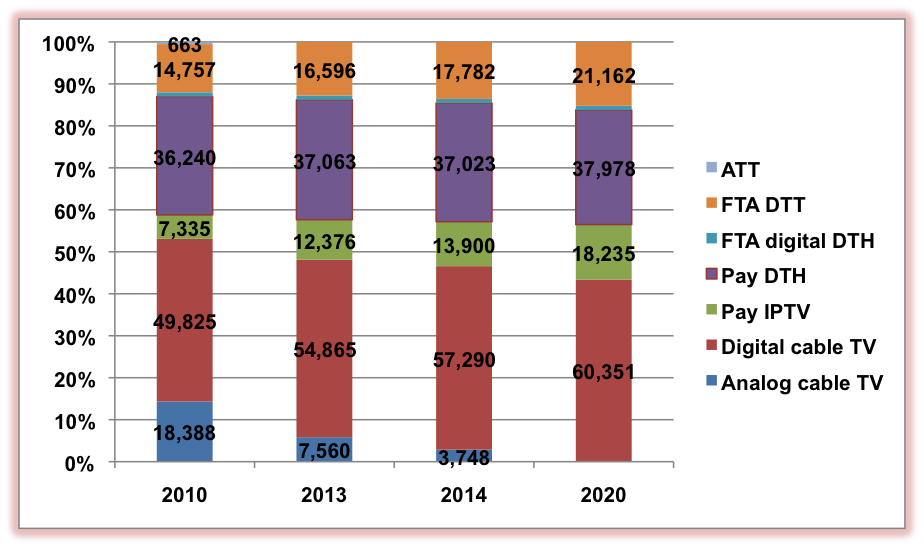

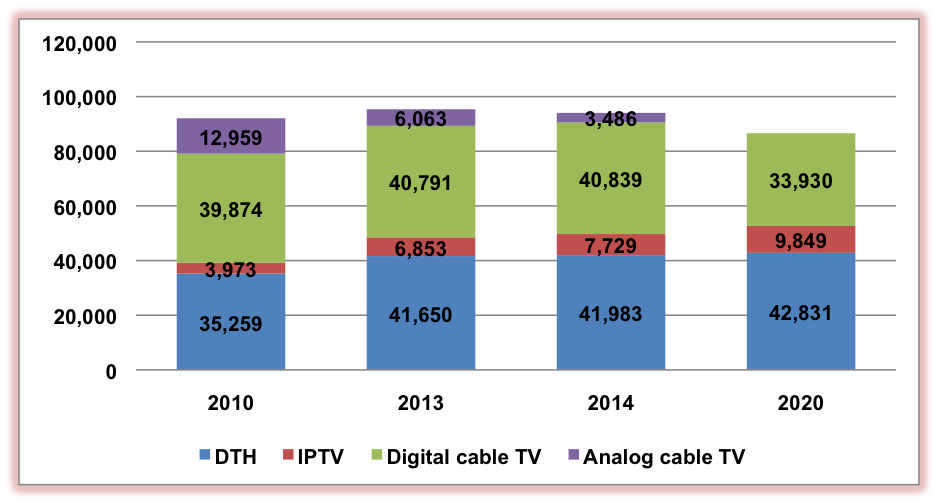

Most of the pay TV subscriber losses over the last few years have been analog cable subs. There were still 18.39 million analog cable subscribers by end-2010, a number that will fall to 3.75 million by end-2014.

North America: Share of TV households by platform (000)

Digital TV penetration reached 94.2% at end-2013, and will increase to 100% by 2017 – the only remaining analog homes take cable. Of the 17 million digital homes to be added between 2013 and 2020, 5.5 million will come from cable, 5.9 million from IPTV, 4.6 million from DTT and 0.9 million from satellite TV.

Digital TV penetration reached 94.2% at end-2013, and will increase to 100% by 2017 – the only remaining analog homes take cable. Of the 17 million digital homes to be added between 2013 and 2020, 5.5 million will come from cable, 5.9 million from IPTV, 4.6 million from DTT and 0.9 million from satellite TV.

Digital TV penetration reached 94.2% at end-2013, and will increase to 100% by 2017 – the only remaining analog homes take cable. Of the 17 million digital homes to be added between 2013 and 2020, 5.5 million will come from cable, 5.9 million from IPTV, 4.6 million from DTT and 0.9 million from satellite TV.

Digital TV penetration reached 94.2% at end-2013, and will increase to 100% by 2017 – the only remaining analog homes take cable. Of the 17 million digital homes to be added between 2013 and 2020, 5.5 million will come from cable, 5.9 million from IPTV, 4.6 million from DTT and 0.9 million from satellite TV.

Pay TV penetration has peaked in Canada and the US. Despite falling pay TV penetration, the number of pay TV subscribers will climb by nearly 5 million between 2013 and 2020 to 116.6 million. Subscriber numbers fell slightly in 2013.

North America pay TV revenues (US$ million)

Simon Murray, Principal Analyst at Digital TV Research, said: “Pay TV revenues [subscriptions and on-demand] in North America peaked in 2013 at $95.36 billion. We forecast that they will fall by $8.75 billion to $86.61 billion in 2020. As the analog cable networks switch off, all pay TV operators will try to outdo each other on promotions, with pricing becoming a more and more important tool.”

Simon Murray, Principal Analyst at Digital TV Research, said: “Pay TV revenues [subscriptions and on-demand] in North America peaked in 2013 at $95.36 billion. We forecast that they will fall by $8.75 billion to $86.61 billion in 2020. As the analog cable networks switch off, all pay TV operators will try to outdo each other on promotions, with pricing becoming a more and more important tool.”

TV ARPU is being forced down as cable operators and telcos convert their subscribers to double-play or triple-play bundles, although blended [overall] ARPU is rising.

Satellite TV will overtake cable to become the largest pay TV platform revenue generator in 2015. However, satellite TV revenues will climb by only $1.2 billion between 2013 and 2020 – to $42.8 billion.

There will be 60.4 million cable homes (all digital) by 2020, down from 62.4 million in 2013 (of which 7.6 million were analog) and 68.2 million in 2010 (18.4 million analog). Cable penetration will be 43.4% by 2020, down from 48.1% at end-2013 and 53.1% in 2010.

Cable revenues will fall by nearly $13 billion between 2013 and 2020 – dropping by $2.5 billion in 2014 alone. Analogue cable revenues will be zero by 2017, down from $13 billion in 2010.

Although many analogue cable subs will convert to digital cable, other platforms, particularly IPTV, will also benefit. Most telcos have already conducted aggressive pricing promotions. Although there has been a recent slowdown in IPTV subscriber growth, the number of homes paying for IPTV will climb by 47% between 2013 and 2020 to reach 18.2 million – or 13.1% of TV households. IPTV revenues will increase at a similar rate to achieve $9.85 billion by 2020.

For more information on the Digital TV North America report, please see the Broadband TV News webshop.

No comments:

Post a Comment